Legacy System Integration and Incompatible Technology Stacks: The Hidden Technical Separation Costs Destroying PE Returns

Why legacy system incompatibility remains invisible until post-close, and how integration complexity compounds across technical, financial, and organizational dimensions.

When a PE firm acquires a carve-out from a corporate parent, it inherits not a standalone company but a collection of deeply entangled legacy systems, incompatible technology stacks, and architectural decisions optimized for a large enterprise rather than an independent operating entity. The business has been running as a cost center within a larger parent—its ERP system is a module of the parent’s SAP installation, its customer data lives in a corporate CRM that serves 10 other business units, its financial reporting is embedded in a consolidated Excel consolidation model that links to systems from four different eras, and its infrastructure lives on corporate servers in a data center shared with dozens of other divisions.

On Day 1 post-close, the carved-out entity must instantaneously become independent. It needs its own ERP system. Its own CRM. Its own financial reporting infrastructure. Its own IT organization. Yet none of these systems were designed for separation. The integration complexity is profound, the costs routinely explode far beyond initial estimates, and the integration timelines extend 12-24 months longer than projected—if they complete at all.

Research on 50+ divested businesses found separation costs ranging from 1% to 5% of divested revenues, with complex carve-outs reaching 13% of revenues. For a $300M revenue carve-out, this represents $3M-$39M in separation costs—often exceeding the entire first year’s EBITDA improvement target. For a PE firm acquiring a carve-out and modeling the deal on achieved separability by Month 9, discovering that integration will extend to Month 24 translates to an 18-month value creation delay that can reduce projected returns by 12-18% in net present value terms.

This article deconstructs the hidden technical separation costs in PE carve-out acquisitions: why legacy system incompatibility remains invisible until post-close, how integration complexity compounds across technical, financial, and organizational dimensions, what specific systems create the highest separation costs, and how to identify and mitigate these risks before the deal closes.

The Carve-Out Technical Separation Problem: Why Legacy Systems Create Catastrophic Complexity

The Fundamental Mismatch: Enterprise Systems Optimized for One Purpose, Carve-Outs Requiring Another

When a corporate parent deploys an ERP system, it optimizes for the parent company’s operational model. A pharmaceutical company’s ERP might be configured to track drug compounds across 12 manufacturing facilities, manage complex regulatory approvals across 30 countries, and consolidate financial results from 50 cost centers. A manufacturing conglomerate’s ERP might handle procurement from 200 suppliers across 15 regions, manage complex inter-company transactions, and track costs through highly detailed allocation models.

When a business unit is carved out from that parent, it cannot simply take its “piece” of the ERP system and operate independently. Enterprise systems aren’t modular in that way. They’re tightly integrated. Financial data flows from the ERP into a consolidated general ledger that’s shared across the enterprise. Customer data stored in the CRM is linked to contracts managed in a document management system that’s also shared. Inventory in one location is tracked in the same database as inventory in seven other locations operated by different business units.

The mathematical reality: separating a business unit from an integrated enterprise system typically requires replicating 80-100% of the enterprise system’s functionality to achieve standalone operations. The buyer doesn’t get to keep 20% of the ERP and use 80%—they have to replicate nearly the entire system for their business unit’s specific needs.

The Three Fundamental Integration Scenarios: Each Creating Different Complexity

Separating business units from enterprise systems requires one of three technical approaches, each with different costs and risks:

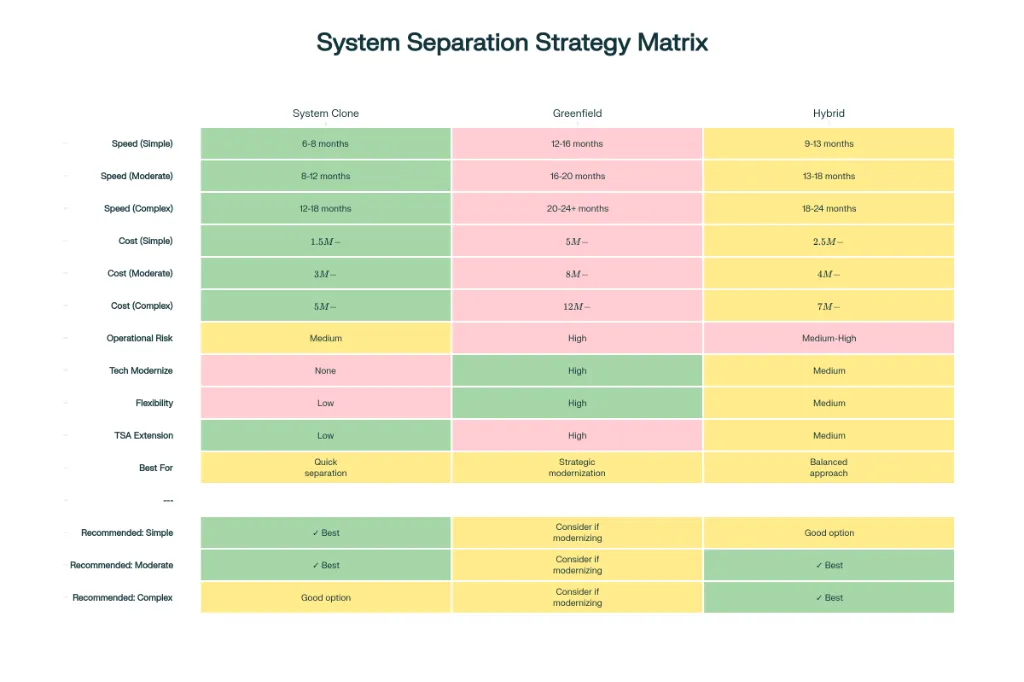

Scenario 1: System Clone (Most Common)

The buyer receives a complete copy of the parent’s ERP system at close, with data isolated to the carved-out business only. This preserves all functionality and business logic but requires:

- Creating a separate ERP instance (licensing costs: $500K-$3M annually depending on system)

- Cloning the entire database infrastructure (setup and validation: $500K-$2M)

- Migrating 3-5 years of historical data (data extraction, cleansing, validation: $200K-$800K)

- Replicating custom code, configurations, and extensions unique to the business unit (if 1,000 hours or more of customization exists, costs reach $300K-$1M+)

- Establishing new security architecture and access controls (infrastructure setup: $150K-$500K)

- Testing to ensure all functionality works identically post-separation (QA and testing: $300K-$1M)

Total system clone cost: $1.5M-$8M Timeline: 6-12 months from deal close Risk: High—if data migration has errors, financial reporting is compromised until discovered and corrected

Scenario 2: Greenfield Implementation (Most Expensive)

Rather than cloning the existing system, the buyer implements a new ERP system designed for the carved-out entity’s business model. This is attractive because it enables modernization (moving from old technology to cloud-based systems) but requires:

- New ERP licensing and subscription (annual: $500K-$2M)

- Complete business process redesign (consulting: $1M-$3M)

- System configuration and customization to match the business (implementation: $2M-$8M)

- Data migration from legacy systems to new system (data engineering: $500K-$2M)

- Full organizational training and change management (training: $200K-$800K)

- Extended parallel operations (running old and new systems simultaneously until transition complete: $300K-$1.5M in extra infrastructure and support)

Total greenfield cost: $5M-$18M Timeline: 12-24 months from deal close Risk: Very High—new systems often have implementation delays, and the parallel operating period extends costs. McKinsey research shows 30-50% of anticipated M&A value is lost due to slow or ineffective integration

Scenario 3: Hybrid Integration (Most Pragmatic)

The carved-out entity receives a clone of the necessary ERP modules while implementing a new system for non-critical functions, using middleware to integrate them. This balances speed with modernization but creates integration complexity:

- System clone of critical modules ($1M-$3M as above)

- New system implementation for targeted functions ($1M-$4M)

- Middleware and integration platform setup to connect systems ($300K-$1M)

- Ongoing integration maintenance and monitoring ($150K-$300K annually)

Total hybrid cost: $2.5M-$8M Timeline: 9-18 months Risk: Medium-High—integration points become failure modes if not carefully managed

The Incompatibility Crisis: When Systems Were Never Designed to Separate

The most insidious technical problem: many carve-out separations face situations where systems are fundamentally incompatible with separation.

Scenario A: Shared Database Architecture

The parent company operates multiple business units on a single, consolidated ERP database where data from all units is stored in the same tables with different “company codes” or “business unit” fields. Separating Company A from this database requires:

- Cloning the entire database (to avoid corrupting parent’s data)

- Identifying all records belonging to Company A (which may be spread across 100+ tables with complex interdependencies)

- Removing parent and sibling company data

- Testing that financial reports, inventory counts, customer records—all critical data—is accurate

- Validating that no data references to parent company remain (which would break after separation)

A single error in this process—deleting a record that should have been retained, or retaining a record that should have been deleted—corrupts the entire standalone system. Companies have discovered months post-separation that they deleted 18 months of customer records, or retained supplier data from a parent company supplier that no longer serves the carved-out entity.

Scenario B: Shared Code Base

The parent’s ERP system contains custom code (business logic written specifically for the company) that serves both the parent company and the carve-out. Separating requires:

- Identifying which custom code belongs to the carve-out vs. parent

- Extracting it into a separate codebase

- Testing that it works identically in the new environment

- Managing any code dependencies that reference shared functionality

For a complex ERP with 2,000+ custom code programs, this process can extend 6-12 months and cost $500K-$2M. During this time, any ERP upgrades or patches must be applied to both old and new systems, creating a fragile dual-maintenance nightmare.

Scenario C: Shared Infrastructure and Data Centers

The carved-out entity’s systems run on hardware in the parent company’s data center using infrastructure controlled by parent IT. Post-separation, the entity needs:

- New data center capacity or cloud infrastructure ($300K-$1M upfront)

- Network separation (firewalls, security groups, VPNs: $100K-$500K)

- Disaster recovery and backup infrastructure independent of parent ($200K-$800K)

- IT operational capabilities (monitoring, incident response, security: $2M+ annually)

Establishing independent infrastructure before separation is critical—but delaying it post-separation creates extended dependency on parent company IT for every outage, every patch, every change.

The Hidden Cost Explosion: Why Separation Estimates Consistently Underestimate Reality

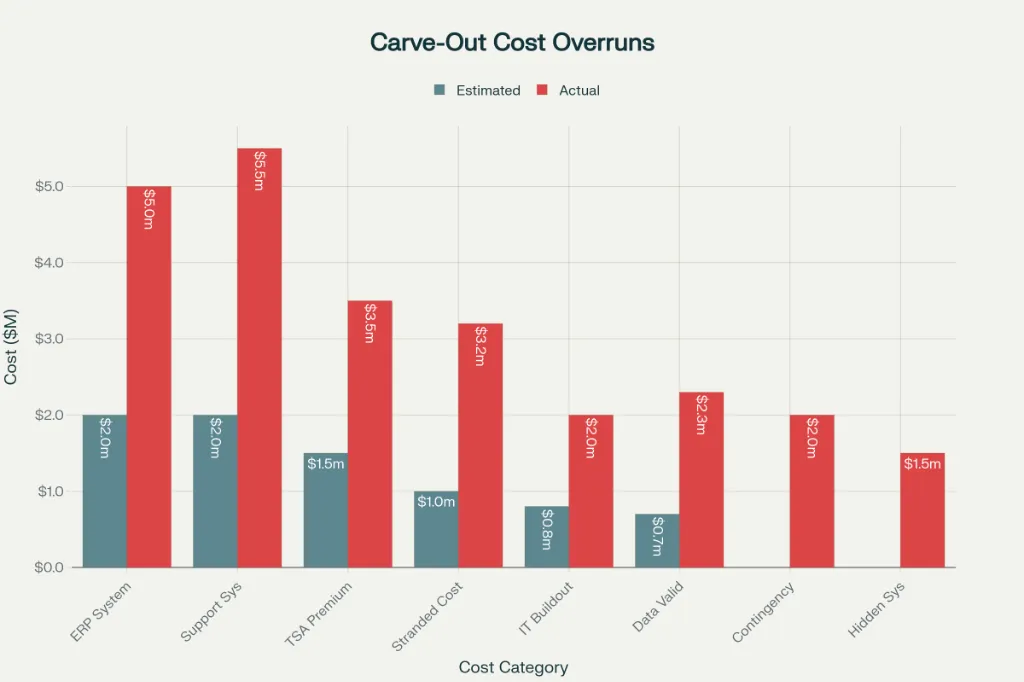

PE firms and sellers typically create initial separation cost estimates during diligence that prove wildly optimistic. The typical pattern: Initial estimate of $2-3M in separation costs becomes $5-8M by completion. Why?

Reason 1: Stranded Costs and Shared Service Allocations

In the parent company’s financials, numerous costs are shared across multiple business units. “Corporate IT” salaries might be allocated 15% to the carve-out. “Finance team” cost might be allocated 10% to the carve-out. “Facilities” might be allocated 5% to the carve-out.

These allocations almost never reflect the cost of truly standalone operations. A corporate IT team serving 10 business units costs $10M annually. If one business unit is allocated 10% ($1M) in the parent’s P&L, does it cost only $1M to give that business unit independent IT? Absolutely not—the business unit now needs:

- IT leadership and governance (CIO, IT director, IT manager: $300K-$500K)

- Infrastructure management (network, servers, cloud: $200K-$400K)

- Applications support (ERP, CRM, specialized systems: $300K-$600K)

- IT security and compliance (security engineer, identity management: $200K-$400K)

- Help desk and user support (helpdesk staff, IT technician: $150K-$300K)

Total independent IT cost: $1.15M-$2.6M

Yet the parent’s allocation said IT would cost only $1M. The “hidden” IT cost is $150K-$1.6M annually. Over a typical 3-4 year separation period, this represents an additional $450K-$6.4M in unexpected costs.

Similar dynamics apply to finance, HR, procurement, and legal functions. Sellers typically underestimate standalone overhead by 20-40% to make carve-out valuations more attractive. Buyers discover post-close that the business requires substantially more overhead than the parent’s cost allocations suggested.

Reason 2: Hidden System Dependencies and “Dark Matter” Systems

During carve-out diligence, PE firms typically identify the “known” systems: the ERP, CRM, and major operational applications. But most large enterprises operate with dozens of “dark matter” systems—older systems, specialized applications, departmental tools—that run quietly in the background serving specific functions.

A typical carve-out might identify 8-12 “critical” systems during diligence, but discover 30-40 systems during detailed separation planning. These dark matter systems include:

- Specialized manufacturing systems (MES, PLM systems used by engineering)

- Supply chain systems (supplier portals, procurement platforms)

- Financial systems (asset management, fixed asset systems, payroll systems)

- Operational systems (customer service systems, field service management)

- Reporting and analytics systems (data warehouses, BI platforms)

- Historical systems (legacy systems that should be decommissioned but are still running)

For each dark matter system discovered, the question becomes: does the carved-out entity need it? If yes, how does it separate? The median cost to separate a single system: $200K-$500K. If 20 dark matter systems exist, this adds $4M-$10M in unforeseen separation costs.

Reason 3: Transition Service Agreement (TSA) Escalation

A Transition Services Agreement allows the seller to continue providing services to the carved-out entity for a defined period (typically 6-12 months) while the buyer builds independent capabilities. TSAs seem reasonable during diligence—“We’ll have 12 months to separate IT, finance, HR, and legal.”

In practice, TSAs become the most expensive and problematic aspect of carve-outs.

Problem 1: TSA Pricing

Sellers typically price TSAs as “cost-plus” arrangements, recovering their cost of providing the service plus a margin (15-30%). For finance processing that costs the parent $200K to provide, the TSA price is $230K-$260K—premium pricing for a service that should be temporary.

For IT infrastructure that costs the parent $500K to host (amortized across 10 business units), hosting the carved-out entity might cost $100K. But the parent, realizing it must maintain infrastructure for the carve-out anyway, often price it as $150-200K, recovering their cost plus margin.

Accumulated across all services, a carve-out with a $5M annual cost structure might incur $6-7M in TSA costs for the same services for one year. Over an 18-month TSA period, this represents an additional $1.5-3.5M in separation costs.

Problem 2: TSA Dependency Extension

Many carve-outs project they’ll be ready to exit TSAs by Month 12. In practice, separation of systems typically extends to Month 18-24. Once Month 12 arrives, the buyer doesn’t have the independent capability in place to take over. They must extend the TSA—extending dependency on the seller and extending costs.

Extended TSAs create a perverse incentive: sellers have strong motivation to delay knowledge transfer or slow-walk capability transition to extend the TSA revenue stream.

Problem 3: TSA Operational Risk

During the TSA period, the carved-out entity’s operations depend on the seller providing services. If the seller experiences an outage, the carved-out entity is impacted. If the seller decides to prioritize other work over the TSA service, the carved-out entity has limited leverage—the seller controls the infrastructure.

A manufacturing carve-out’s production planning system failed during its TSA period due to parent company IT maintenance work. The failure extended 48 hours, creating a production stoppage that cost $500K in lost output. The buyer had to accept this operational risk because they had no independent capability.

Reason 4: Integration Complexity Multiplication

When a carve-out combines system clone (for ERP) + greenfield implementation (for CRM) + TSA extension (for finance), the total complexity multiplies rather than adds.

The cloned ERP requires data migration from the parent instance. The greenfield CRM requires data migration from the parent instance. But the ERP and CRM must integrate—customer master data exists in both systems, and the two systems must share the same customer definitions. If CRM customer ID “12345” doesn’t match ERP customer “CUST-12345”, orders don’t route properly and financial reporting breaks.

Resolving these integration points requires custom development, testing, and often rework when initial integration efforts fail. A carve-out that planned for independent ERP + independent CRM discovers that they need $1-2M in integration work to make the systems talk to each other—work that wasn’t anticipated in the initial separation budget.

The Financial Impact: Quantifying System Separation Costs

For PE firms evaluating carve-out opportunities, the financial impact of legacy system complexity can be quantified across several dimensions:

Direct Separation Costs

For a typical $200-300M revenue carve-out from a large technology or manufacturing parent:

| Cost Category | Low Estimate | High Estimate |

|---|---|---|

| ERP system clone/greenfield | $1.5M | $8M |

| CRM and customer data separation | $500K | $3M |

| Supporting systems separation (20+ systems) | $2M | $8M |

| Infrastructure and data center setup | $500K | $2M |

| TSA premium over normal service costs (18 months) | $1M | $4M |

| Data validation and remediation | $300K | $1.5M |

| IT organization buildout and staffing | $1M | $3M |

| Total First Year Separation Costs | $7.3M | $29.5M |

For a $250M revenue business with typical 15% EBITDA margins ($37.5M EBITDA), separation costs of $7.3-29.5M represent 20-79% of first year EBITDA. For carve-outs that modeled value creation around margin expansion targets of $5-10M, separation costs consume or exceed the entire margin expansion budget.

Stranded Cost Absorption

Beyond direct separation costs, the carved-out entity must absorb stranded costs that were previously allocated to parent:

| Function | Parent Allocation | Standalone Cost | Hidden Cost |

|---|---|---|---|

| Finance (CFO, controller, accounting staff) | 8% × $5M = $400K | $1.5M-$2.5M | $1.1M-$2.1M |

| IT (infrastructure, applications, support) | 10% × $10M = $1M | $2M-$3M | $1M-$2M |

| HR and Legal | 5% × $3M = $150K | $800K-$1.2M | $650K-$1.05M |

| Facilities and Occupancy | 12% × $4M = $480K | $1M-$1.5M | $520K-$1.02M |

| Total Annual Stranded Costs | $2.03M | $5.3M-$8.2M | $3.27M-$6.17M |

Over a 5-year hold period, stranded cost absorption totals $16.35M-$30.85M in additional baseline overhead that wasn’t anticipated in the carve-out operating model. For a business modeled on 15% EBITDA margins, these stranded costs reduce margins to 10-12%, impairing returns.

Timeline Impact and Value Creation Delay

The most significant financial impact: carve-out integration delays extend the time required to achieve value creation targets.

A typical carve-out might model:

- Month 6: Separation complete, TSA exited, independent operations achieved

- Month 12: Margin expansion initiatives 50% complete; EBITDA improved by $3M

- Month 24: Margin expansion initiatives 100% complete; EBITDA improved by $8M

- Month 36+: Ready for exit at target multiple

In practice, the timeline typically extends:

- Month 12-18: Separation finally complete after discovering hidden systems and stranded cost requirements

- Month 24: Margin expansion initiatives delayed due to IT team focused on separation; EBITDA improved by only $1-2M

- Month 36: Margin expansion initiatives accelerating; EBITDA improved by $5-6M

- Month 42+: Ready for exit (12-18 months delayed vs. plan)

This timeline delay has massive financial impact. For a carve-out valued at 7x EBITDA ($56M × 7 = $392M entry valuation) targeting 12x exit EBITDA ($112M × 12 = $1.344B exit), the difference between Month 36 exit and Month 42 exit is:

- Month 36 exit: $1.344B valuation; 3.4x MOIC over 3-year hold

- Month 42 exit: $1.344B valuation (but achieved 6 months later); 2.9x MOIC over 3.5-year hold

The value creation is identical, but the time required extends 17% longer, and the annualized return (MOIC / years held) declines from 1.13x per year to 0.83x per year—a meaningful degradation in returns on an already marginal PE deal.

For more aggressive PE portfolios targeting 3.5-4x returns over 5 years, a 12-18 month integration delay often makes the deal uneconomical.

The Vendor Lock-In Amplifier: Why Legacy Systems Create Additional Separation Costs

Beyond integration complexity, legacy system separations are often complicated by vendor lock-in dynamics that increase separation costs.

Oracle Lock-In: The $2.5M Cautionary Tale

Oracle has built its licensing model around making exit expensive. Oracle licensing is processor-based (using “core factor” calculations specific to Oracle’s proprietary assessment). When a company is on Oracle and wants to move to a different database system:

- The company must export all data from Oracle into a vendor-neutral format

- The data often requires transformation to match the new database’s structures

- Custom code using Oracle-specific syntax must be rewritten

- Integration points using Oracle-specific APIs must be rebuilt

- Licensing agreements often include clauses restricting data export, creating legal risk

A U.S. manufacturer on Oracle, during carve-out separation, attempted to migrate to a cloud-based system. Oracle’s licensing agreement restricted data export. The company faced a choice:

- Negotiate with Oracle for permission to export (at higher licensing costs)

- Pay the “migration penalty” Oracle embedded in their license

- Remain on Oracle in the cloud

The company ultimately spent $2.5M to migrate away from Oracle—a cost entirely driven by Oracle’s contractual and technical lock-in.

SAP Legacy Lock-In: The ECC Crisis

SAP’s widely-installed ERP system “SAP ECC” (the legacy version) will reach end-of-support in 2025. Companies running SAP ECC—including many carved-out entities—face a critical choice: migrate to SAP S/4HANA (the modern cloud version) or continue on unsupported legacy software.

Carve-outs from large manufacturing or pharmaceutical companies often run on SAP ECC because the parent operates on ECC. When a carve-out is separated, inheriting the cloned ECC system, it immediately faces a dilemma: invest $10-20M to migrate to S/4HANA now, or operate on unsupported legacy software post-exit.

This creates a forced modernization investment that wasn’t anticipated in carve-out models. PE firms acquiring a carve-out on SAP ECC must either:

- Budget $10-20M for S/4HANA migration during hold period

- Accept technology and security risk post-exit by remaining on unsupported software

- Negotiate with the seller for a purchase price reduction to fund the migration

Most PE firms discover this issue too late—only after the carve-out is separated and operational.

Custom Code Lock-In: The “Business Logic Trapped in Legacy Systems” Problem

Many legacy ERP systems contain 1,000-5,000 hours of custom code representing specific business logic that the company has built over years or decades. This custom code is often written in outdated programming languages (ABAP for SAP, PL/SQL for Oracle) that few modern developers understand.

During carve-out separation, this custom code must either:

- Be replicated to the new ERP (if separating to a new system)

- Migrate unchanged (if cloning the system)

- Be rewritten to work with a modern system (if modernizing during separation)

For option 1 (replication): Rebuilding 2,000 hours of custom code in a new platform costs $500K-$1.5M and takes 6-9 months. For option 2 (migration): The custom code travels with the cloned system, continuing to lock the carved-out entity into legacy technology. For option 3 (rewrite): The cost and timeline extend 12-18 months.

A pharmaceutical carve-out inherited custom code representing production scheduling logic worth $2-3M in operational value. This logic had been refined over 10 years and was critical to manufacturing efficiency. During separation, the carve-out discovered that replicating this logic to a modern system would require $1.5M in development and a 9-month timeline. The alternative—remaining on the legacy system—preserved the functionality but locked the business into obsolete technology.

Integration Failure Case Study: When Separation Timelines Explode

A real-world example illustrates how legacy system complexity creates integration failure:

The Software-as-a-Service Carve-Out

A large technology company carved out a SaaS business unit that had been operating as an internal division. The carve-out’s financials showed:

- $50M ARR in revenue

- $12.5M EBITDA (25% margin)

- 18-month projected integration timeline

- $3M projected separation costs

Initial Assessment Identified:

- ERP system (clone from parent SAP ECC)

- CRM system (Salesforce instance shared with parent)

- Finance system (consolidated into parent’s Oracle general ledger)

- Product database (shared cloud infrastructure)

Pre-Close Underestimation: The buyer assumed 6 months to clone and separate the SAP system, 6 months to establish independent Salesforce and finance infrastructure, and 6 months to establish independent product database and cloud infrastructure.

Post-Close Reality:

- Month 1-3: Data mapping and validation discovers that the carve-out’s data is fragmented across the parent’s systems. Customer data lives in Salesforce. Customer configuration data lives in the ERP. Customer billing data lives in Oracle. Customer usage data lives in a specialized analytics database. No system serves as single source of truth.

- Month 4-6: Attempting to clone SAP reveals 2,000+ customizations specific to the carved-out business unit, plus another 1,000+ customizations shared with parent that must be untangled. The carve-out’s code references parent company’s data in ways that break upon separation.

- Month 6-9: Discovering “dark matter” systems: a specialized customer provisioning system (not mentioned in carve-out diligence), a billing system (legacy, running on infrastructure parent IT manages), and a reporting system (Excel-based consolidation that pulls from 6 different systems). Each discovery adds $200-500K in separation cost.

- Month 9-12: CRM separation proves more complex than anticipated. Salesforce uses custom fields and workflows specific to parent company’s operations. Extracting the carved-out entity’s data and reconfiguring Salesforce for standalone operations requires more customization than budgeted. The work extends through Month 15.

- Month 12-15: Oracle separation discovers that the carved-out entity’s financial data is intermingled with parent’s data in ways that don’t cleanly separate. The finance controller had consolidated 18 months of historical data, and extracting the carved-out entity’s subset requires restatement and validation.

- Month 15-18: TSA extension becomes necessary because independent capabilities aren’t ready. Instead of exiting at Month 12, the buyer must extend TSAs through Month 24 (adding $2-3M in unexpected costs).

- Month 18-24: First major incident: discovered after separation that $500K in customer payments from Month 4 were not properly migrated to the new billing system. The payments exist in the old system but aren’t reflected in the new system’s accounts receivable. Resolution requires manual reconciliation and re-entry.

- Month 24+: Finally achieving independent operations, but 12 months behind schedule. The business has been in crisis mode for 6 months, operating with divided attention between integration and operational execution. Value creation initiatives were deferred due to integration focus.

Financial Impact:

- Projected separation cost: $3M

- Actual separation cost: $9.5M (+$6.5M or 216% overrun)

- Projected integration timeline: 18 months

- Actual integration timeline: 24+ months (+6 months delay)

- Value creation delay: Originally targeted Month 18 exit readiness; delayed to Month 30+ (12 month delay)

For a carve-out valued at 8x EBITDA ($100M entry value targeting $150M+ exit value), the 12-month delay in achieving operational maturity and readiness for value-creation initiatives reduced exit timing from Year 3.5 to Year 4.5—compressing overall MOIC from an anticipated 2.8x over 3.5 years to approximately 2.2x over 4.5 years.

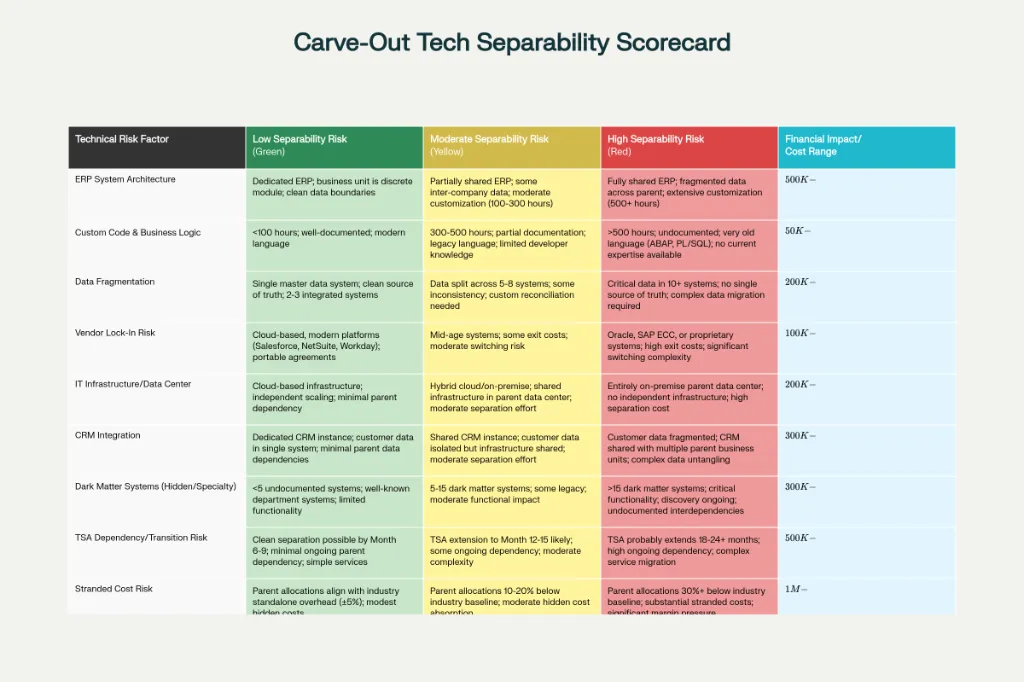

Assessment Framework: Identifying Legacy System Risk During Diligence

For PE firms evaluating carve-out acquisitions, identifying legacy system risk requires going beyond standard IT due diligence to assess separability complexity.

Phase 1: System Landscape Mapping (Week 1-2)

Activities:

- Map all systems the business unit currently uses

- Identify which systems are dedicated to the business unit vs. shared with parent

- Document data flows between systems

- Identify data consolidation points (where data from multiple systems is brought together)

Output: System dependency map; shared vs. dedicated system inventory

Phase 2: Separation Feasibility Assessment (Week 3-4)

Activities:

- For each shared system, assess options: clone, greenfield, or TSA during transition

- Estimate cost and timeline for each option

- Identify “dark matter” systems that might exist

- Assess custom code complexity and customization extent

- Evaluate vendor lock-in risks (Oracle, SAP, etc.)

Output: Preliminary separation roadmap; cost estimates for each option

Phase 3: Detailed Technical Assessment (Week 5-6)

Activities:

- Interview IT leaders about hidden dependencies

- Request architecture documentation and system designs

- Assess data quality and completeness of data that will be separated

- Evaluate existing TSA provisions and service level commitments

- Review vendor agreements for exit penalties and lock-in clauses

Output: Detailed technical separation plan; identified risks and mitigation strategies

Phase 4: Financial Modeling (Week 7+)

Activities:

- Build detailed separation cost model with 3 scenarios (low, mid, high complexity)

- Model stranded cost absorption and standalone overhead

- Project timeline impact on value creation

- Calculate revised IRR under different separation scenarios

Output: Revised deal model accounting for separation costs; risk-adjusted valuation

Red Flags: When Legacy System Complexity Should Kill the Deal

Certain technical characteristics should raise serious concerns about carve-out separability:

Red Flag 1: “We Don’t Know” Responses If the seller cannot clearly explain what systems the carve-out uses, how they’re shared with parent, or what customization exists, separation will be extremely expensive. Lack of clarity signals fragmented, legacy, poorly documented systems.

Red Flag 2: Large Custom Code Base If the business unit has more than 500 hours of custom code in legacy systems, the cost to replicate or modernize that code during separation will exceed $250K-$500K. For highly customized systems, this reaches $1-2M+.

Red Flag 3: Extreme Data Fragmentation If customer data lives in 4+ different systems and no system serves as single source of truth, carve-out separation will face data migration challenges that extend timeline and inflate costs by $1-3M.

Red Flag 4: Stranded Cost Underestimation If allocated parent costs are significantly lower than typical standalone overhead (e.g., IT allocated at 5% but industry standard is 12-15%), the carved-out entity will face substantial stranded cost absorption.

Red Flag 5: Vendor Lock-In If the business unit operates on Oracle, SAP ECC, or other legacy systems with known exit costs, factor $500K-$3M in modernization or migration costs into the deal model.

Red Flag 6: Complex Inter-Company Transactions If the carve-out has significant transactions with parent company (inter-company sales, shared services agreements, allocation of corporate costs), the financial separation will be complex and stranded costs will be substantial.

Recommendations for PE Firms

1. Invest in Rigorous Technical Carve-Out Due Diligence

Allocate budget and timeline for specialized technical assessment focused specifically on separability, not just IT controls. This should include:

- System architecture review

- Custom code analysis

- Data quality assessment

- Vendor lock-in evaluation

Cost: $75K-$200K Timeline: 3-4 weeks ROI: Prevents $3-10M+ in unexpected separation costs

2. Create a Technology Carve-Out Reserve

Rather than modeling separation costs as a discrete line item, create a 30-50% contingency reserve in the separation budget. Typical reserves:

- Small/simple carve-out ($100-200M revenue): 30% reserve

- Moderate carve-out ($200-500M revenue): 40% reserve

- Large/complex carve-out ($500M+ revenue): 50% reserve

Example: For a $3M base estimate, add $900K-$1.5M reserve, resulting in $3.9M-$4.5M true separation budget.

3. Front-Load System Separation in Deal Timeline

Rather than attempting to separate all systems simultaneously after close, conduct logical separation planning pre-close:

- Identify which systems can be cloned immediately vs. which require extended TSA

- Develop detailed separation roadmap with clear milestones

- Establish clear accountability for each separation workstream

- Budget for external support (system integration partners) for complex separations

4. Evaluate Strategic Technology Modernization Alongside Separation

Rather than treating modernization (e.g., SAP ECC to S/4HANA migration) as a separate future project, evaluate whether modernization should be bundled with separation:

- Modernizing during separation adds cost but enables greenfield design optimized for the independent company

- Delaying modernization locks the business into legacy technology longer

- Calculate 5-year TCO for “migrate now during separation” vs. “migrate later as standalone”

5. Establish Clear TSA Exit Criteria

Structure TSAs with clear, measurable exit criteria rather than fixed durations:

- TSA for ERP: Exit when new ERP achieves stable state and passes reconciliation testing

- TSA for finance: Exit when independent finance team closes monthly financial statements on schedule

- TSA for IT infrastructure: Exit when dedicated infrastructure is operational and passes disaster recovery testing

Clear exit criteria create accountability and prevent indefinite TSA extension.

6. Build Technical Separation Governance

Establish dedicated carve-out management office with clear ownership:

- Carve-Out Program Lead (executive-level accountability)

- System Separation Workstream Leads (for each major system)

- Cross-functional coordination (finance, IT, operations)

- Weekly progress reviews and escalation protocols

Conclusion: Legacy Systems as the Hidden Value Destroyer in Carve-Outs

The technical complexity of separating legacy systems from parent company infrastructure is the hidden value destroyer in PE carve-out acquisitions. While PE firms typically assess revenue, margins, and competitive position during diligence, technical separability remains poorly assessed—often treated as a discrete line item in IT budgets rather than a fundamental risk to deal economics.

The firms that will outperform in carve-out investing are those that:

- Invest in rigorous technical diligence assessing separability complexity

- Build realistic separation budgets with appropriate contingency reserves

- Treat technology integration as part of the core value creation plan, not as a support function

- Establish clear governance and accountability for separation execution

- Recognize that technology modernization opportunities exist within carve-out separations, not just risks to manage

For PE firms, CFOs of carved-out entities, and integration leaders, treating legacy system integration as a strategic value creation lever—rather than a peripheral IT project—is essential to achieving carve-out returns.

The difference between carve-outs that achieve projected returns and those that underperform often comes down to whether leadership recognized that legacy system separation costs, timeline, and complexity are inseparable from the fundamental business economics of the deal.

References and Source Data

- BCG analysis of 50+ divestitures and carve-outs; separation costs range from 1-5% of revenues, reaching 13% in complex cases (2023-2025)

- McKinsey research on M&A integration: 30-50% of anticipated value is lost due to slow or ineffective integration (2023)

- FTC Consulting analysis of carve-out financial separations; sellers reduce projected overhead costs by 20-40% in standalone entity models (2025)

- U.S. manufacturer ERP vendor migration case study; total migration costs $2.5M driven by Oracle licensing restrictions and vendor lock-in (2023-2024)

- Additional sources: PitchBook Q1 2024 PE Middle Market Report (carve-out prevalence); BCG “Learning to Love ERP Migrations in Private Equity” (2025); McKinsey “Operations: The Alpha Factor in PE Carve-Out Deals” (2025); Panorama Consulting on ERP interoperability challenges (2024); iFD PE Carve-Out Financial Challenges (2025); E78 Partners Carve-Out best practices (2025); NetSuite implementation cost analysis (2025); SAP S/4HANA migration benchmarks (2% -4% of revenue); Boston Consulting Group “Don’t Let Carve-Out Costs Compromise Value Creation” (2023)